Grant Administration: Tax Credit Basics

What is the New Hampshire Community Development Tax Credit – CDFA gives a 75% state tax credit against a donation made to any approved project. The tax credit may be applied against the New Hampshire Business Profits Tax (BPT), Business Enterprise Tax (BET), and/or the Insurance Premium Tax. Businesses have up to 5 years to claim the credit after the pledge payment is made. Donations may be made in the form of cash (this is most common), securities or real estate. Please contact CDFA directly if a donor will be using securities or real estate.What types of businesses participate in the Tax Credit Program – Any business that pays the BPT, BET or IPT. Some examples include, but are not limited to, banks, insurance companies, manufacturers, automobile dealers and small local businesses. CDFA will not refer a project to a specific donor but has provided a list of businesses which have participated in CDFA’s tax credit program by way of the CDFA Annual Report.

Are CDFA tax credits eligible for a federal charitable deduction – Once a contribution is received, CDFA will send the business a combined state and federal charitable contribution letter. A business may be eligible for a partial federal tax deduction. But every business’s tax situation is different. The donor is responsible for determining if they are eligible for a federal deduction and should consult a tax professional.

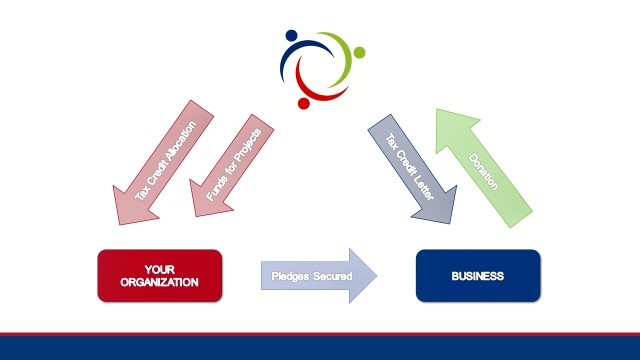

How does the Tax Credit process work – The process for an organization to receive funds through the tax credit program is a cooperative partnership between the organization, a donating business and CDFA.

Step 1: CDFA awards an organization a tax credit allocation

Step 2: The organization secures pledges from NH businesses

Step 3: The business submits its donation to CDFA

Step 4: CDFA provides the business with tax credit letter documenting the donation.

Step 5: CDFA retains a 20% program fee on donations for administration.

Step 6: Funds for projects are available to be released to the project once fundraising has been completed in accordance with the contract.

Tax Credit Pledge Agreement – The tax credit pledge is a binding agreement between a donor and CDFA that spells out the terms under which the donor business promises to make an investment into a project in exchange for the tax credit. The business will need to provide the following information:

- The total gross pledge amount.

- The date(s) that the pledge (A business may select more than one payment date) will be paid based on the state fiscal year of the tax credits your project has available.*.

- Contact information for the business and the organization.

- The pledge also has sections to complete if donor wants to have invoices and/or the tax credit donation letter sent to a different department.

* Tax Credit Year vs. Business Calendar Year – Tax Credits are issued on based on the State Fiscal Year which runs from July 1 – June 30. However, the fiscal year for many businesses is based on a calendar year (January 1 – December 30). Please note that when a business provides a pledge payment date, it will be for the State Fiscal Year of the tax credit donation NOT the Business Calendar Year. They will not necessarily be the same. Please contact the CDFA Project Manager assigned to the project if clarification is needed.

Online Pledge Form – CDFA strongly suggests that donors use our online pledge portal for ease of use. It can be accessed at http://www.nhcdfa.org/electronic-pledge.

Paper Pledge Form – If a donor prefers a paper pledge it can be found on the tax credit resources page http://www.nhcdfa.org/tax-credits/tax-credit-resources under the Donor Information link. Please follow directions for submission on the pledge form for submission.

Claiming the Tax Credit – After the donor business pays the pledged amount to CDFA the business will receive a combined state/federal tax credit letter from CDFA confirming payment of the pledge and the date after which the state tax credit can be taken. A business filing for the credit will use state form DP160 at https://www.revenue.nh.gov/forms/all-forms.htm. A business may “carry forward” the credits in full or in part for up to five years until fully claimed. Please note that contributors are responsible for consulting with their own tax credit advisors to determine the financial impact of contributing to the CDFA tax credit program.